What happens next for mining equities - recovery or dead cat bounce?

Published: April 5, 2016

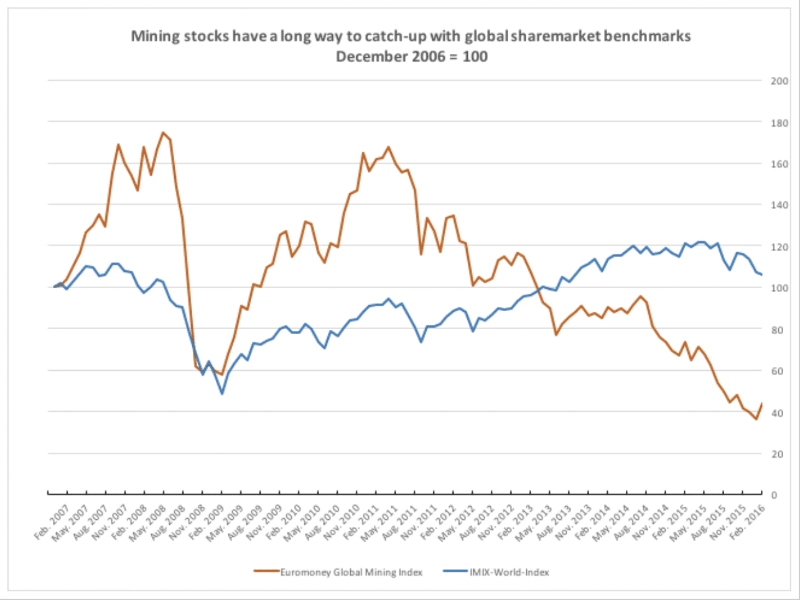

Figure 1. Performance of Mining Equities vs General Equity Markets

The Euromoney Mining Index covers 152 mining stocks across 24 markets and is a good proxy for mining sector equity prices. The EMIX World Index is highly representative of global equities across all sectors and cover approximately 85% of the free float capitalisation of developed markets.

Figure 1 tracks the relative performance of the two indexes over the last ten years. Mining stocks as measured by Euromoney Global Mining Index is down some 70% over the past five years while gross returns are a negative 65%. The broader equities market as measured by the EMIX World Index is up approximately 24% while gross returns are up around 41%. Clearly as every resources investor knows, the last five years have been miserable for the mining sector.

But there are some early but subdued signs of the mining sector equity prices approaching bottoming and of possible recovery. The Euromoney Mining Index is showing more than 20% recovery since the beginning of this year. This compares favourably with the wider market which is flat year to date.

At the Mine Insider we are firm believers that there is a difference between the intrinsic value of a company or asset and its market price. As the great value investors, such as Warren Buffet, tell us, it is the difference between market price and intrinsic value which create profitable investment opportunities. It is critical that the investor should be arriving at a clear view about intrinsic values as distinct to market prices. Our discussion today is primarily about market prices.

Against this nascent recovery in mining equity prices is a chorus of analysts voicing that the current recovery will be short-lived and share prices will fall below January lows. The general consensus of the analysts’ community is that further falls in minerals prices are needed until sustained supply cuts are made by miners which will then provide price support.

At the Mine Insider we are more sanguine. Barring a Black Swan event we don’t expect a boom, but we hold with our earlier forecast that mineral commodity prices may have found bottom. Some of the factors that the Mine Insider considers to reach this forecast include continuing wage and employment growth in the U.S. and the recovery in residential property prices in China. Furthermore, we are seeing some supply cuts have been instigated for many minerals (although not enough for a boom or to silence the pessimistic analysts).

Which leads us back to the Mine Insiders’ expectations for mining company share prices. Figure 2 shows how the market prices for mining stocks respond to changes in minerals commodity prices. The IMF Metals Price Index tracks movement of Copper, Aluminum, Iron Ore, Tin, Nickel, Zinc, Lead, and Uranium Price Indices.

Figure 2. Movement in Mining Equity Prices vs Minerals Prices

It shows a high correlation between mining equity prices and spot commodity prices. This suggests that investors are not taking a view on long term prices (as they appeared to do in 2007), but instead are simply extrapolating spot prices. Given the industry’s forecasting record this is not a surprise. We have already seen an improvement in mining equity prices since the beginning of the year, during which time the commodity prices are also coming off the bottom.

At the Mine Insider, we think mining equity prices have hit bottom and so buying opportunities are emerging. Already value investors are seeking opportunities with payback over a medium term horizon. But while we think it is now time to invest in commodities, we repeat our caveats from previous posts - as we highlighted in our post ‘The great mining ‘Liquidation Sale’ – time to buy distressed assets?’ :

- You need to be highly selective about the specific investments; and

- You need to to arrive at an independent view on the price you are willing to pay based on long term value.

Curious about how you can leverage marketing to realize the highest returns on investment? Download this white paper for insights about how to optimize your marketing efforts.

This article was originally published at Mine Insider.