The DecisionNext Finished Goods Index Report | May 2026

Published: May 18, 2026

Protein Inflation Is Diverging Ahead of Summer

As summer grilling season approaches, the DecisionNext Finished Goods Index is showing a growing divide across the protein complex.

Cheeseburger costs continue to climb sharply, driven by historically elevated beef prices and persistent tightness in lean-trim markets. At the same time, hot dog prices appear to be stabilizing after significant inflationary pressure over the past year, while chicken sandwich costs are declining amid continued production growth. All bun and bread prices are expected to rise due to higher wheat prices brought on by drought conditions.

The result is a protein and grain market that is no longer moving in one direction.

For procurement teams, retailers, and foodservice operators, that divergence matters. Different protein and grain inputs are now carrying very different pricing risks heading into the summer demand period, creating both challenges and opportunities for merchandising, promotional planning, and purchasing strategy.

The May Finished Goods Index highlights how structural differences across beef, pork, and poultry markets are beginning to reshape the economics of some of America’s most common food items.

Figure 1 – May 2026 Index values and DecisionNext forecasts for May, June, and July.

Key Insights

- Cheeseburger costs continue climbing sharply ahead of peak summer demand, with forecasts pointing to additional upside through July.

- Hot dog costs remain historically elevated but appear to be stabilizing relative to beef-based finished goods.

- Chicken sandwich costs continue to normalize as poultry markets soften from prior-year highs.

- Protein inflation is no longer moving uniformly across categories, creating widening pricing gaps between beef, pork, and chicken.

- Lean beef tightness and elevated trim markets continue to drive disproportionate inflation pressure across burger-related products.

![]()

Cheeseburger Index

The Cheeseburger Index continued moving higher in April as beef-driven inflation accelerated ahead of the summer grilling season.

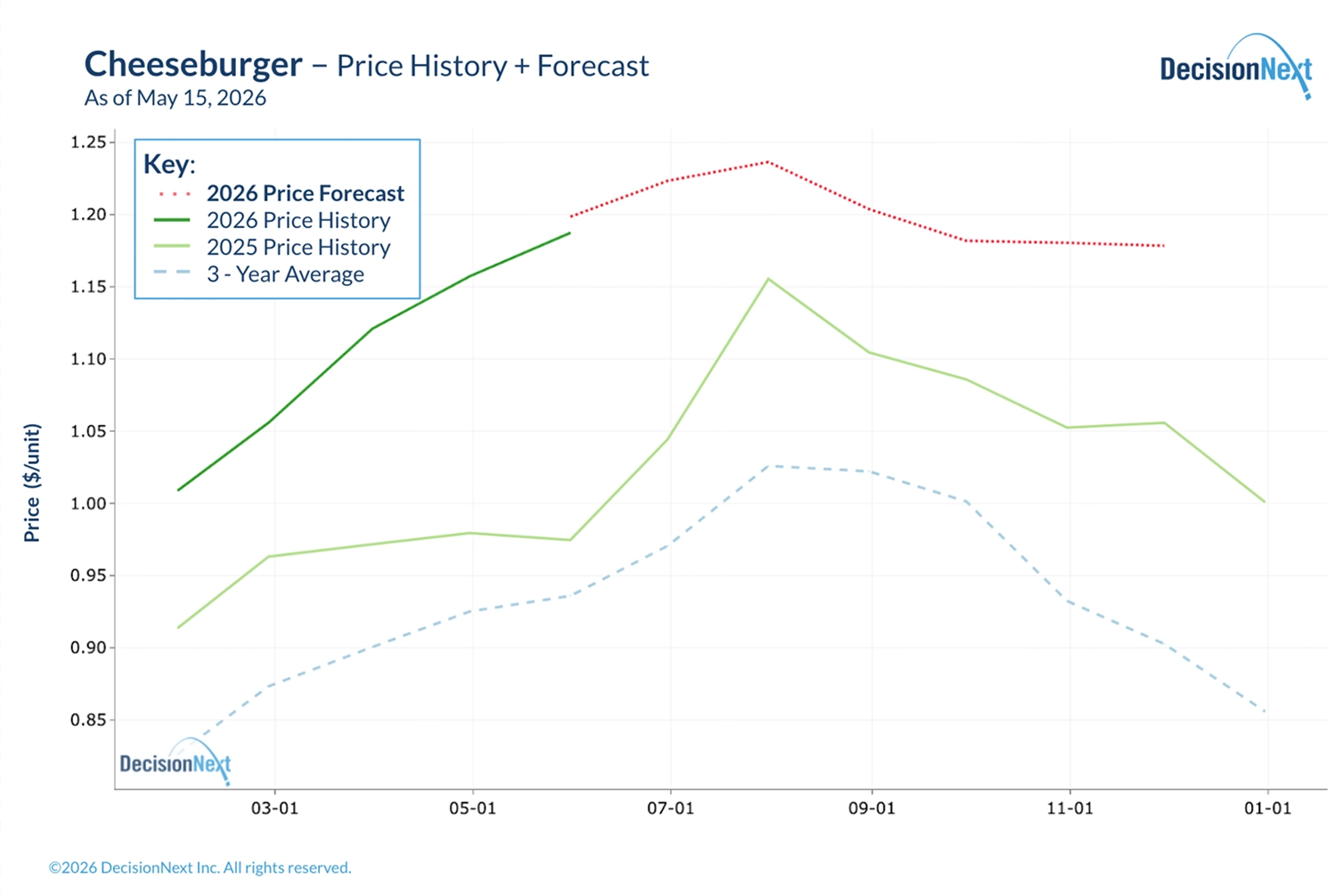

The index is forecasted to reach 117 by end of May, climbing further to 119 in June and 121 in July (Fig. 1). Cheeseburger ingredient costs are projected to rise from $1.20 per serving in May to $1.24 by July, largely driven by the increasing price of lean trim (Fig. 2).

Figure 2 – Cheeseburger price history and 6-month forecast.

![]()

Hot Dog Index

The Hot Dog Index remains elevated historically, but recent forecasts suggest inflationary pressure may be beginning to stabilize.

The index is forecasted to reach 120 by end of May before easing slightly into June and stabilizing through the remainder of the summer forecast period (Fig. 1).

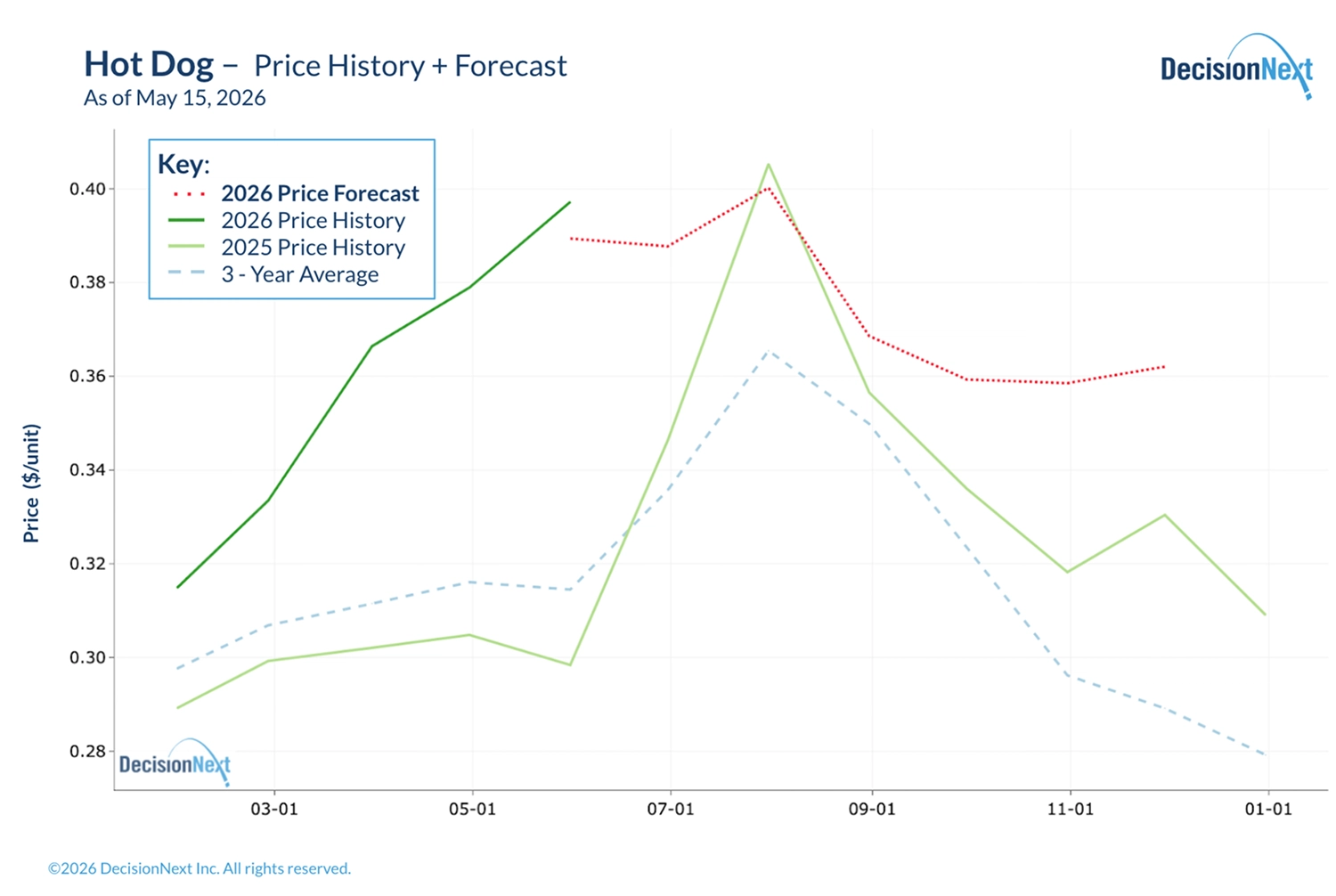

Unlike the cheeseburger market, pork-based finished goods are not currently experiencing the same degree of structural supply tightness. While hot dog ingredient costs remain above historical averages, the market appears to be behaving more normally from a seasonal perspective with prices expected to peak at $0.40 in July, notably below year ago levels (Fig. 3).

Figure 3 – Hot Dog price history and 6-month forecast.

![]()

Chicken Sandwich Index

The Breaded Chicken Sandwich Index continued to trend lower in May as poultry markets normalized from the elevated pricing environment seen throughout much of 2025, driven by continued growth in chicken production volumes.

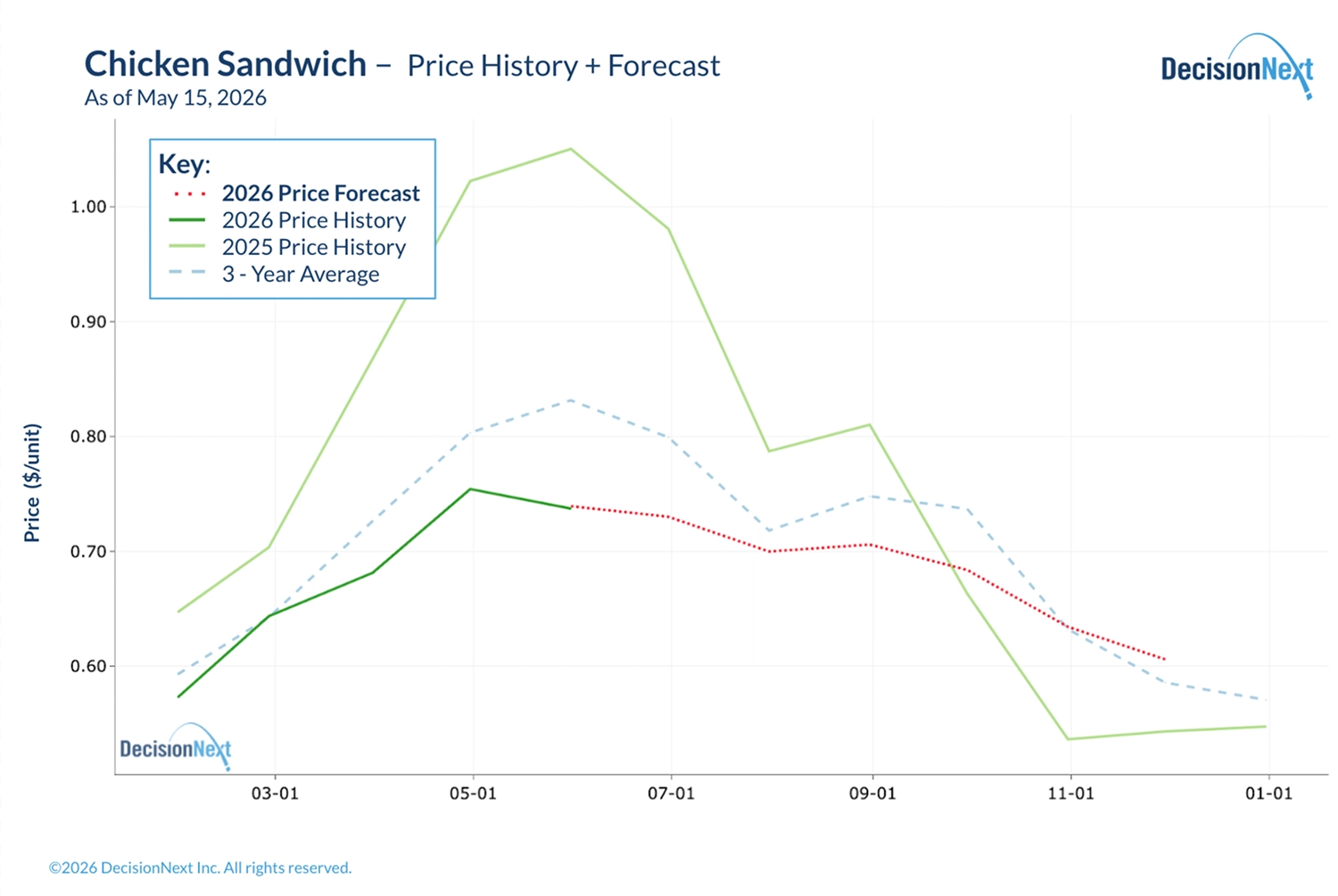

The index declined to 95 in May, with forecasts projecting continued easing through the summer months.

Unlike beef markets, poultry supply conditions have improved significantly, allowing chicken-based finished goods costs to move closer to longer-term averages. Poultry markets are, however, facing increased upside risk from rising concerns of drought conditions across the Western US, which would lead to higher bun costs (through wheat) and higher feed costs, both of which would drive up the chicken sandwich index.

Figure 4 – Chicken Sandwich price history and 6-month forecast.

The Growing Economic Gap Between Beef, Pork, and Chicken

One of the clearest themes emerging from the May Finished Goods Index is that protein inflation is no longer moving uniformly across the market. Beef, pork, and poultry markets are increasingly operating under very different supply conditions, resulting in widening pricing divergence across finished goods categories.

- Beef costs, in particular lean beef grinds, continue accelerating higher as beef markets remain constrained by historically tight cattle supplies and elevated lean trim pricing.

- Meanwhile, pork markets appear comparatively more balanced, allowing hot dog costs to stabilize after prior inflationary pressure.

- At the same time, poultry markets continue normalizing as production conditions improve and chicken prices soften. This could change if higher feed costs drive up chicken costs.

The result is a widening economic spread between some of the most common protein-based food items in the U.S. market.

Implications for Protein Buyers

This divergence carries important implications for both retailers and foodservice operators.

Historically, broad food inflation periods often pushed most protein categories higher simultaneously. Today’s market environment is more fragmented.

That fragmentation creates a more complex operating environment:

- Beef products may require more selective promotions and tighter purchasing management.

- Pork products may offer more stable promotional opportunities.

- Chicken products may increasingly become value-oriented menu drivers.

For consumers, these pricing shifts will undoubtedly influence purchasing behavior.

As cheeseburger costs continue rising, consumers may increasingly shift toward alternative proteins or lower-cost beef occasions. Retail feature activity around chucks vs. middle meats already suggests growing emphasis on value-oriented beef products relative to premium middle meats.

One of the primary drivers behind this divergence remains the lean beef market.

Ground beef production relies heavily on lean trim inputs, including imported lean beef supplies from countries such as Australia, New Zealand, and South America. Recent policy discussions surrounding imported beef quotas have further highlighted the market’s growing sensitivity to lean beef availability and could affect price forecasts.

The broader implication is clear: protein inflation is no longer a single unified story.

Different protein types are now carrying very different pricing risks, creating a market environment where procurement strategy, promotional planning, and menu positioning may increasingly require protein-specific approaches rather than broad inflation assumptions.