Diving into the 50s Trim Market Ahead of Summer

Published: May 18, 2026

Key Insights

- Despite historically elevated prices, current forecasts point toward a relatively flat-to-lower 50% lean trim market through the summer.

- The 50s market behaves more independently than broader beef fundamentals often suggest.

- Heavy formula contracting leaves a limited negotiated supply, increasing the market’s sensitivity to forward buying activity.

- Monitoring negotiated and forward market volumes may provide earlier warning signs than price action alone.

Over the past several weeks, one topic has consistently come up in conversations with customers: the outlook for the 50% lean trim market.

Despite historically elevated price levels and the typical seasonal tendency for summer strength, current DecisionNext forecasts suggest a relatively flat-to-lower 50% lean trim market through the normal summer peak. That outlook has understandably raised questions, particularly after the sharp price spike experienced during the summer of 2025.

Do we really expect it to be flat-to-down through the typical summer peak? Particularly after the spike observed in 2025.

Current answer: yes — for now.

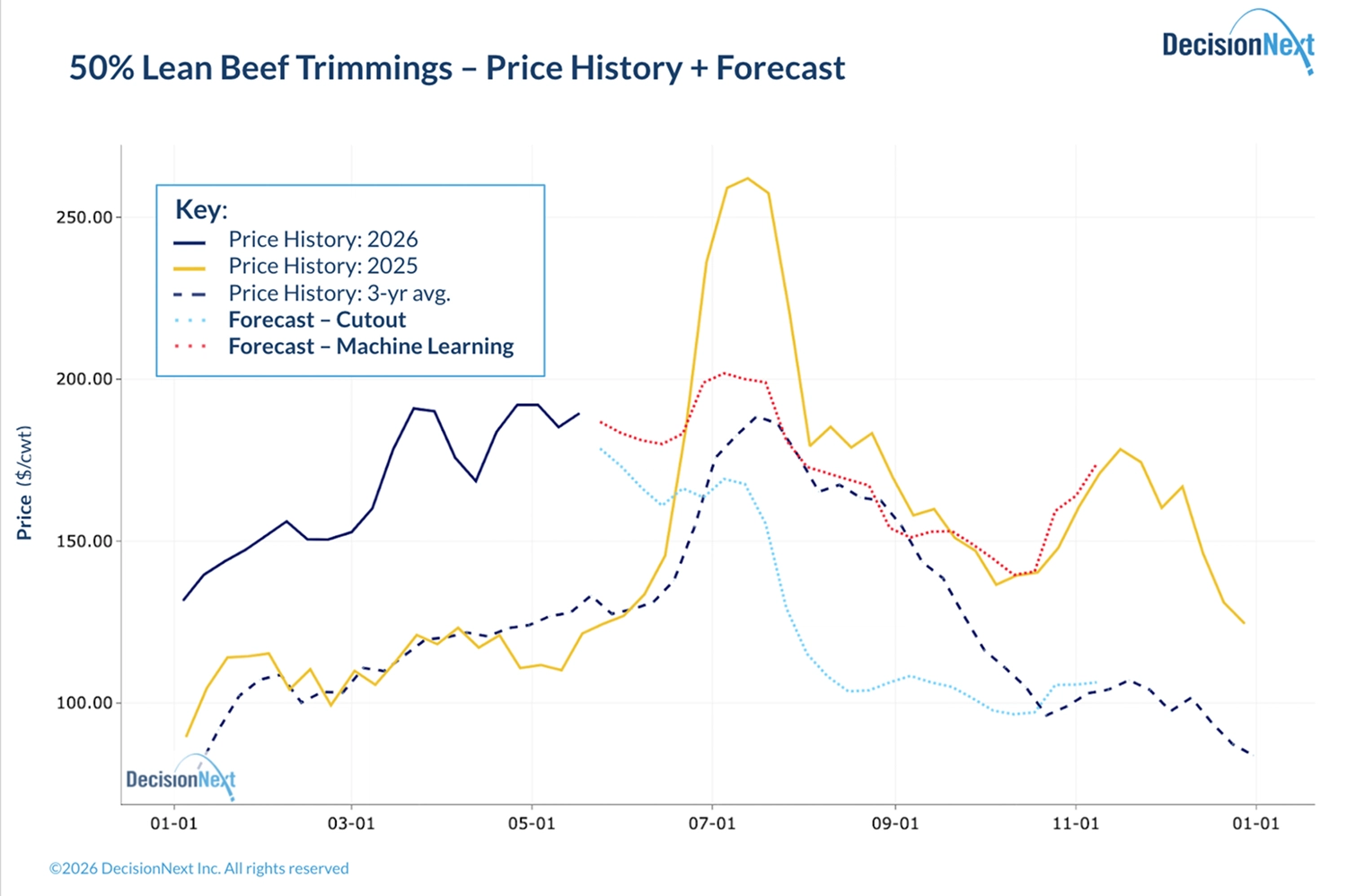

Figure 1 – Forecast for Negotiated 50% Lean Beef Trimmings

Despite 50% lean trim values running well above both last year and the three-year average, the current DecisionNext forecast points toward a relatively flat-to-lower market through the remainder of the summer (Fig. 1). Importantly, the projected summer profile currently sits below the seasonal trajectory implied by the three-year average and well below the extreme spike experienced during the summer of 2025.

That said, this remains a market where conditions can change quickly if forward buying activity accelerates and negotiated supply tightens.

Why the 50s Market Behaves Differently

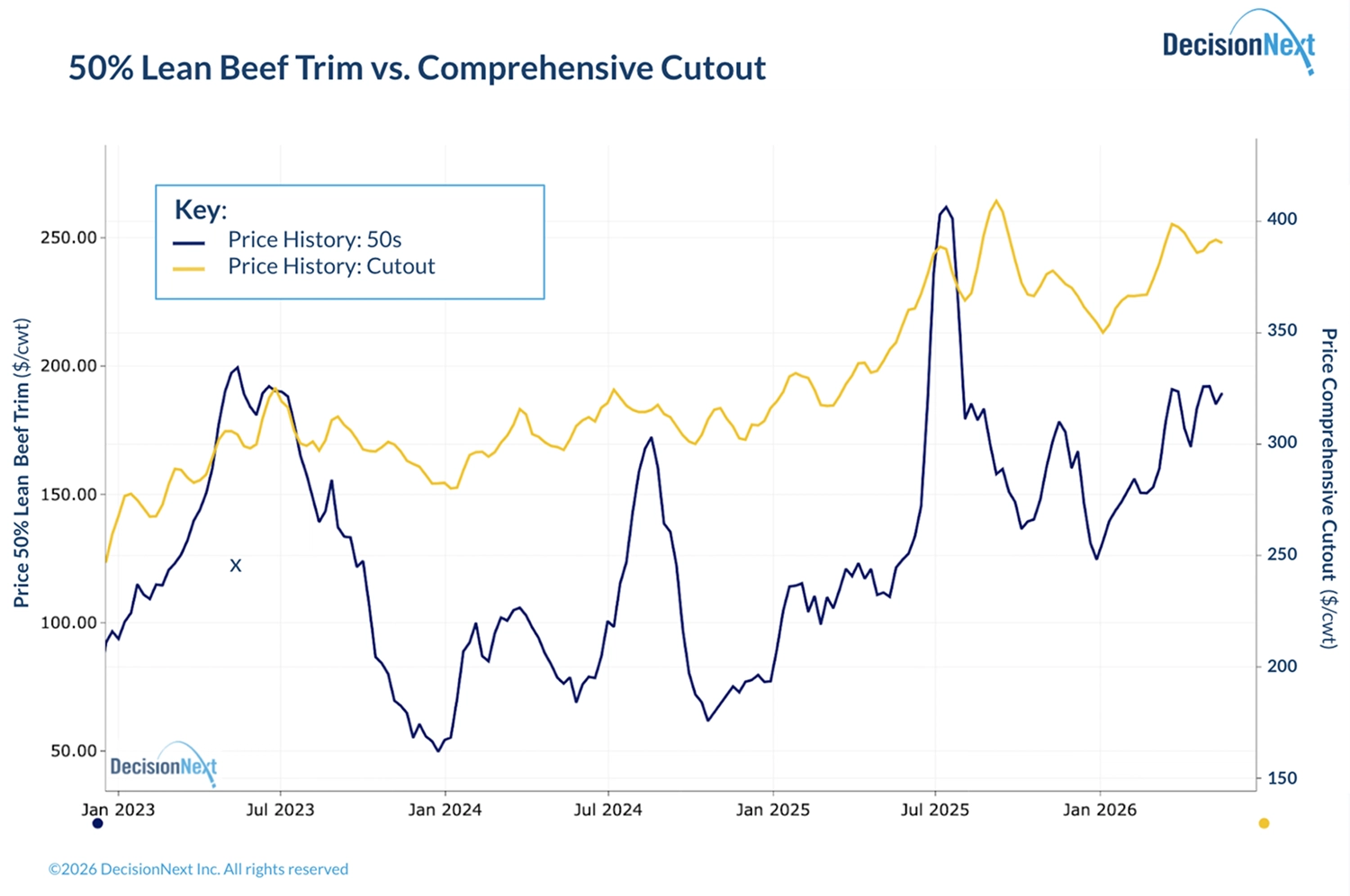

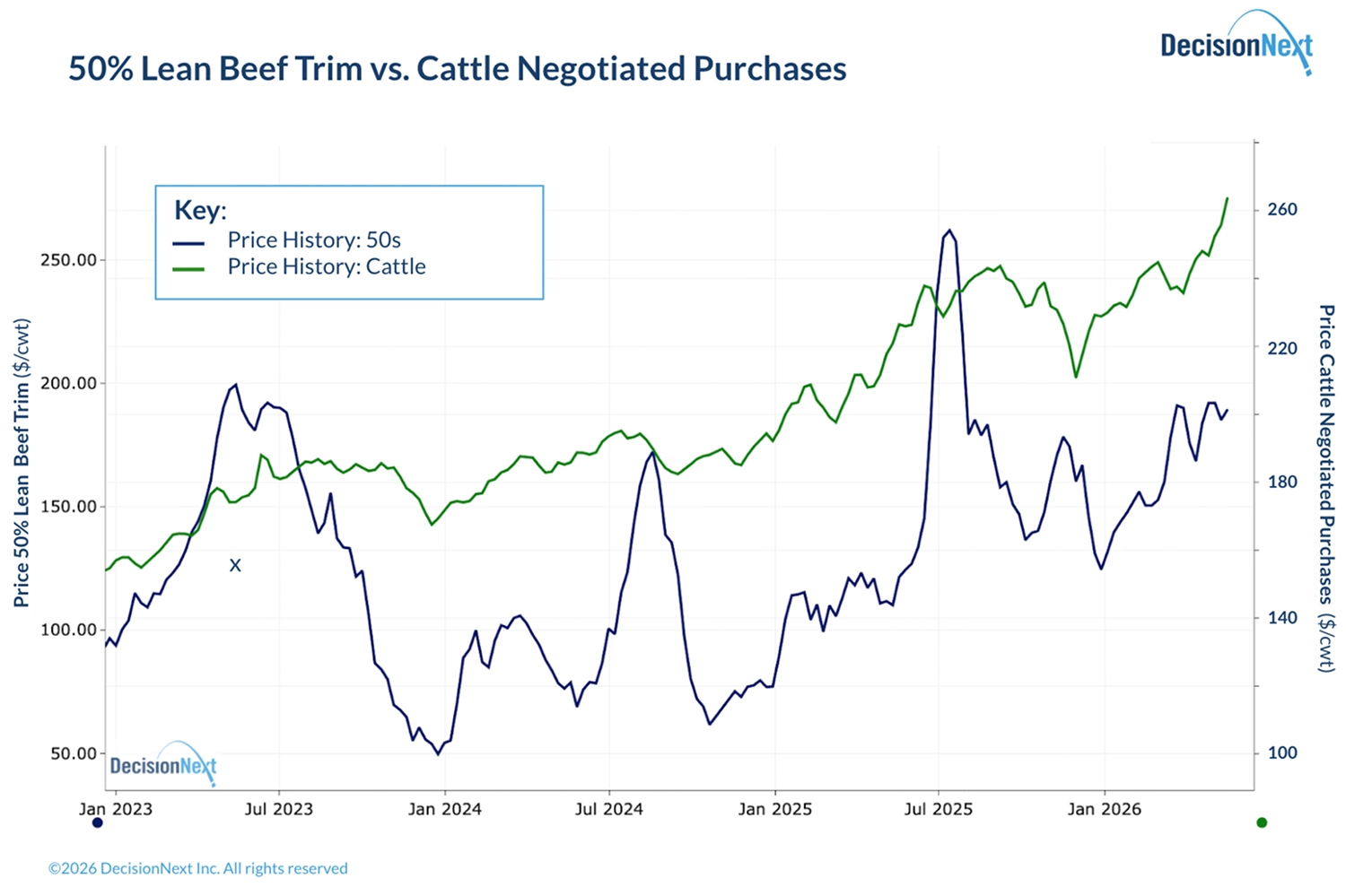

Although 50% lean trim is an important component of the broader beef complex, the market often behaves differently from cattle and cutout values. Figures 2 and 3 compare 50% lean trim prices against both cattle prices and the comprehensive cutout dating back to January 2023.

Figure 2 – 50% Lean Trim vs. Comprehensive Beef Cutout

Figure 3 – 50% Lean Trim vs. Cattle Prices

While 50% lean prices do move alongside broader cattle and cutout trends, the relationship is weaker than many market participants assume. Since 2023, 50% lean trim has shown correlations of 0.52 with cattle prices and 0.61 with the comprehensive cutout.

In fact, 50% lean trim showed a stronger correlation with whole turkey values (0.65) over the same period. Meanwhile, cattle and cutout values themselves maintained a correlation of 0.97.

The implication is important: broader beef fundamentals matter, but they do not fully explain price behavior in the 50% lean trim market.

The Structural Driver Behind 50s Volatility

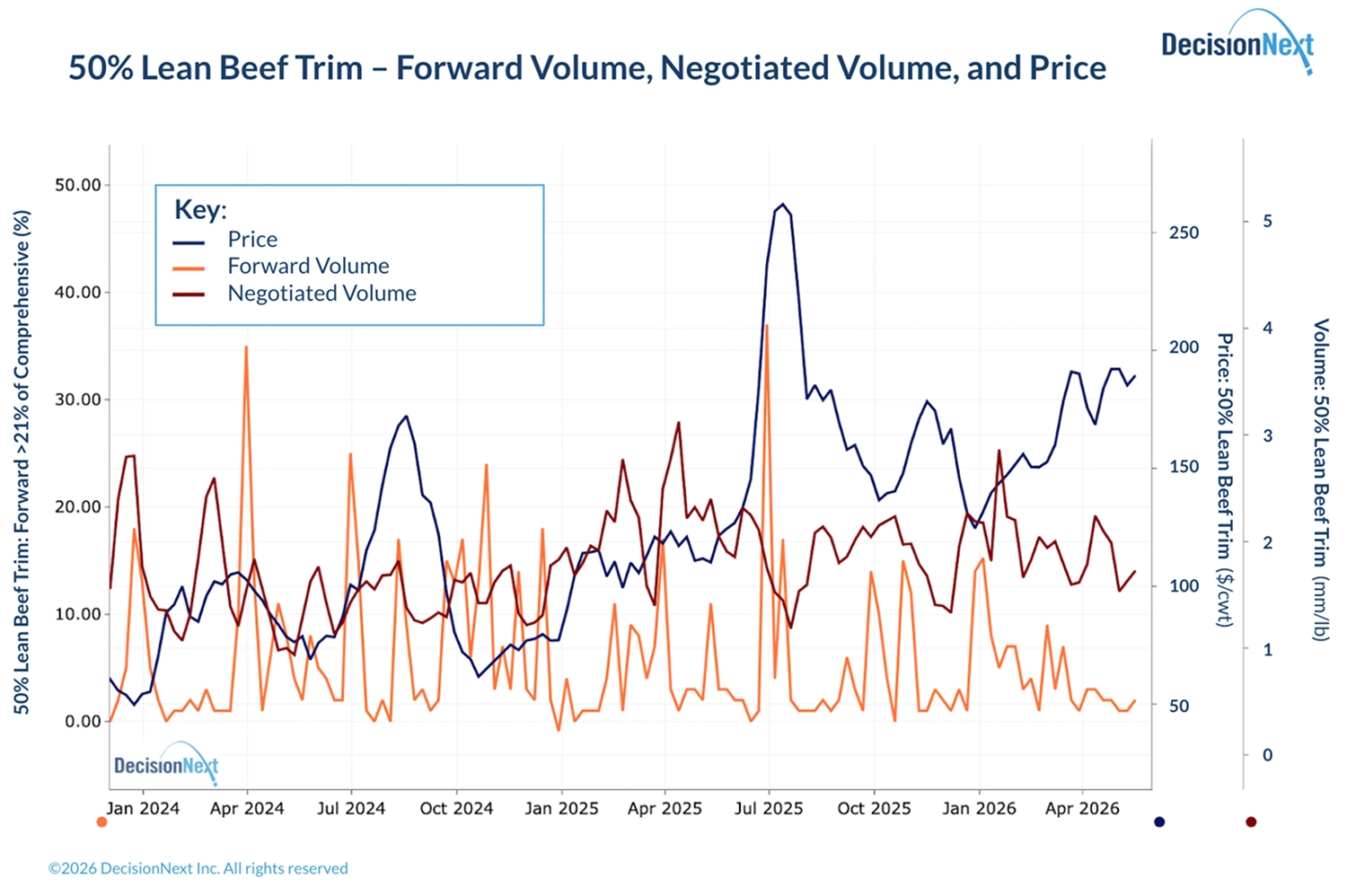

To understand where the market may head next, it is more useful to focus on market structure than on broader beef trends alone. The 50% lean trim market is heavily dependent on formula trade. In fact, only 93% lean ground beef has a higher percentage of formula volume.

Since 2021, approximately half of overall cut volumes have traded on formula. For 50% lean trim, that figure has averaged roughly 82%. This dynamic matters because a market with high committed volume leaves relatively little flexibility in the negotiated spot market. When buying behavior changes unexpectedly, the available supply can tighten very quickly.

As a result, relatively small shifts in forward purchasing activity can create outsized price reactions.

What Happened During the 2025 Summer Spike

During the lead-up to the summer peak of 2025, a large forward purchase — or potentially multiple large purchases — entered the market just as prices were already rising.

As forward activity increased, negotiated spot-market volume declined. With less product available in the spot market, 50% lean prices accelerated even higher.

A similar pattern emerged again during the October-November run-up. Forward buying activity tightened negotiated availability and amplified price movement.

Figure 4 – Forward Volume, Negotiated Volume, and 50% Lean Prices This is why monitoring volume trends is an important complement to the price forecast.

The forecasting model is highly effective at identifying seasonal tendencies and broader market patterns. However, no forecast can fully anticipate sudden behavioral shifts from a small number of large buyers in a structurally tight market.

Looking back at prior market behavior is therefore critical to understanding what drove abnormal price levels — and whether similar conditions may be emerging again.

What Buyers Should Watch Over the Next Six Months

For buyers managing 50% lean exposure over the next six months, two indicators matter most:

- Changes in Forecast Direction Current forecasts continue to support elevated but not extreme prices into August, followed by a gradual decline. However, that outlook remains highly sensitive to changes in forward purchasing behavior.

- Changes in Market Participation and Volume Monitoring negotiated, formula, and forward market volumes may provide earlier warning signs of tightening conditions before they fully appear in price action.

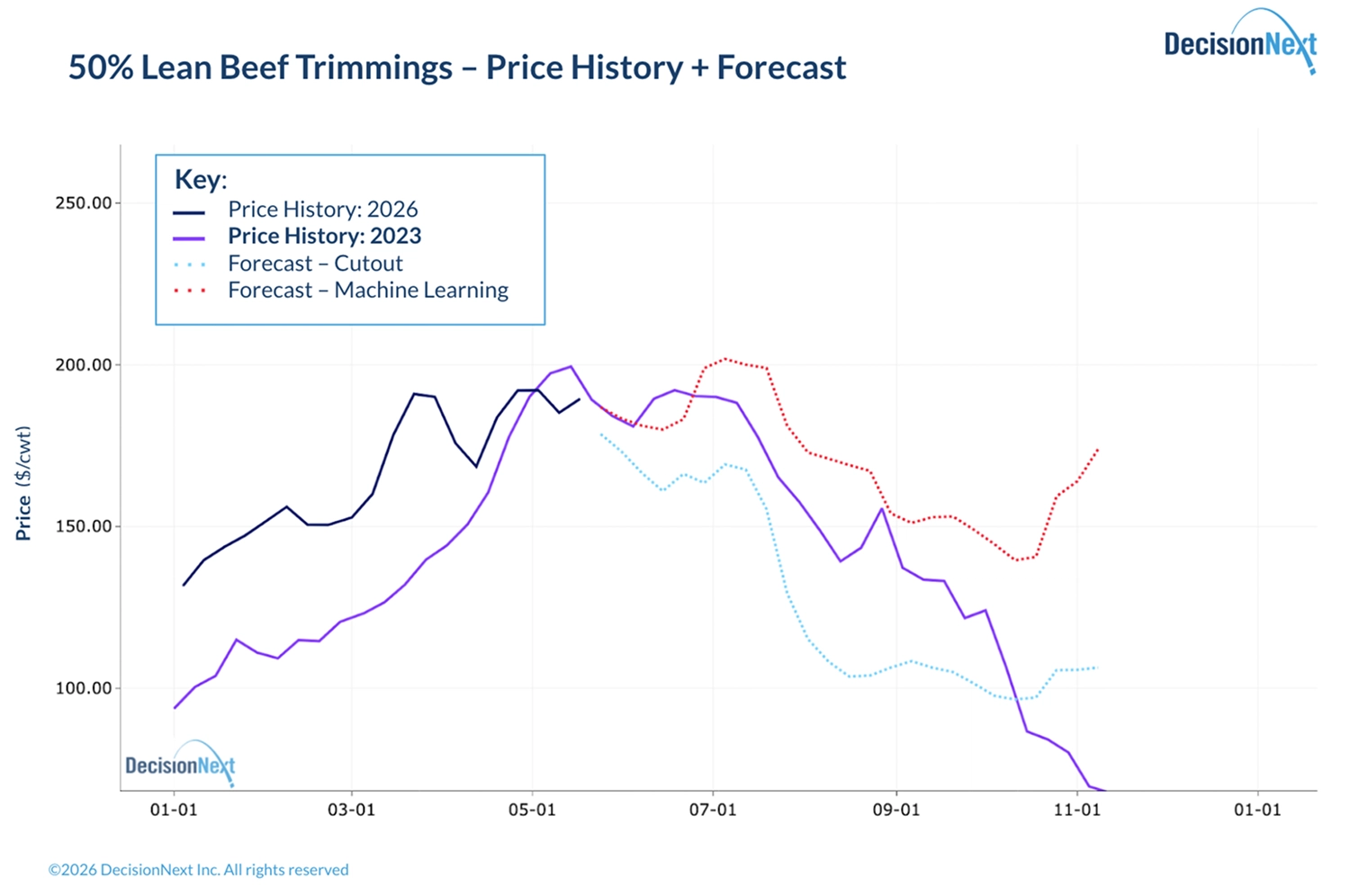

Interestingly, 2023 provides a useful historical comparison. During that year, 50% lean trim values climbed into the summer months but did not experience the same aggressive spike seen in 2025 (Fig 5).

Figure 5 – Price History 2026 compared to 2023. Forecasts: Cutout and Machine Learning models.

Current forecasts suggest a similar possibility for 2026: a market characterized by sustained but manageable price strength rather than an extreme summer rally.

Absent another major forward-buying event that materially tightens negotiated supply, the market is currently expected to remain elevated but relatively orderly before easing later in August.

Closing Takeaway

The key takeaway is that the 50% lean trim market is often driven less by broad beef fundamentals and more by shifts in negotiated availability. As long as forward buying activity remains orderly, current forecasts continue to support a high-but-manageable summer market. But in a structurally tight system with limited negotiated flexibility, liquidity can disappear quickly — and with it, price stability.